Your credit score is one of the most important numbers in your financial life. In Kenya, it determines your ability to access loans, credit cards, mobile lending apps, and even services like Lipa-Pole-Pole. A good credit score not only improves your loan approval chances but can also help you negotiate lower interest rates and better terms.

Unfortunately, many Kenyans either don’t know their credit status or struggle to build it. The good news? With a few consistent steps, you can significantly improve your score over time.

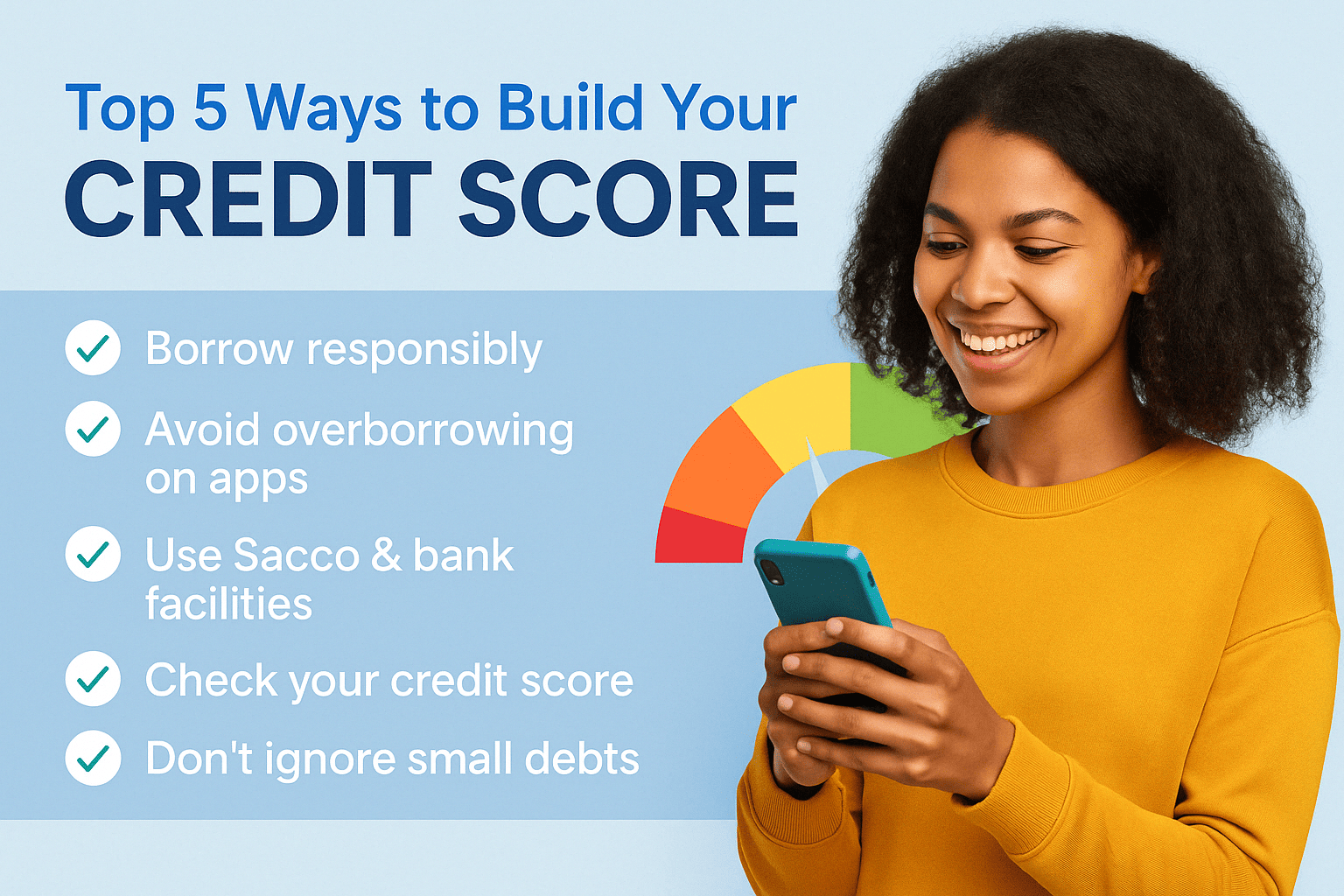

1. Borrow Responsibly and Repay on Time

This is the golden rule. Whether it’s a bank loan, Sacco facility, M-Shwari credit, or Fuliza overdraft—your repayment history is one of the biggest factors affecting your credit score.

- Pay every instalment on time

- Avoid rolling over mobile loans repeatedly

- Even partial payments are better than none

Your repayment habits are tracked by CRBs (Credit Reference Bureaus) like Metropol, TransUnion, and CreditInfo. Regular defaults, especially on small loans, can drastically damage your score.

2. Avoid Overborrowing on Mobile Loan Apps

Kenya's mobile lending space has grown rapidly, with apps like Tala, Zenka, Branch, Okash, and KCB-M-Pesa offering quick loans. While convenient, excessive borrowing from multiple apps within short periods signals credit desperation to lenders.

- Stick to 1 or 2 platforms at a time

- Don’t borrow again before clearing your current balance

- Pay back before the due date—not on the final day

Using too many loan apps simultaneously may lead to over-indebtedness, which lenders view as high risk.

3. Use Sacco & Bank Facilities to Build Credit History

While digital apps dominate, Saccos and banks remain powerful allies in building long-term creditworthiness.

- Saccos allow you to borrow against savings and repay in structured plans

- Banks offer secured personal loans, credit cards, and salary advances

These institutions often report to CRBs and build your profile in a more structured and formal way than mobile apps.

4. Check Your Credit Score Regularly

Did you know you’re entitled to one free credit report every year from any licensed CRB?

Regularly checking your score helps you:

- Track improvement

- Spot errors or outdated information

- Challenge blacklisting that’s been resolved

Visit CRB websites like:

💡 Tip: You can also sign up for SMS updates or download their mobile apps to stay informed.

5. Don’t Ignore Small Debts or Utility Bills

Even seemingly small amounts like:

- Unpaid mobile phone postpaid bills

- School fees arrears

- Hustler Fund or HELB loan defaults

…can negatively impact your credit score.

Always clear pending dues—even if they seem minor. Lenders and CRBs don’t judge based on the amount owed but on the fact of non-payment.

Final Thoughts

Building a strong credit score takes time, discipline, and intentional financial behavior. Don’t wait until you need a loan to start caring about your credit profile. Instead, form good habits now—whether it’s using a Sacco loan, repaying Tala early, or checking your CRB report every quarter.

At Pesa Trends, we help you compare credit products and make smart borrowing choices. Want to improve your loan eligibility? Start by building your score today.